🔹 Introduction

One of the biggest advantages of GST is the ability to claim Input Tax Credit (ITC). ITC allows businesses to set off the GST paid on purchases (inputs/services) against GST collected on sales. For SMEs, startups, and traders, ITC is crucial to reduce tax cost. However, wrong claims can lead to notices, penalties, and blocked credits.

This guide explains ITC in simple, layman-friendly language with practical tips.

(References: Sec. 16–21 of CGST Act, Rule 36, Rule 42/43)

🔹 What is Input Tax Credit?

-

Suppose a trader buys goods worth ₹1,00,000 + 18% GST (₹18,000).

-

He sells them for ₹1,20,000 + 18% GST (₹21,600).

-

He collected ₹21,600 GST from buyer but already paid ₹18,000 GST on purchase.

-

Net liability = ₹21,600 – ₹18,000 = ₹3,600.

✅ This benefit of adjusting purchase tax against sales tax is called Input Tax Credit.

🔹 Who Can Claim ITC?

A registered taxpayer can claim ITC if:

-

They have a valid tax invoice.

-

Goods/services are received.

-

Supplier has filed GSTR-1 and tax is reflected in GSTR-2B.

-

Tax has been paid to the government.

-

GSTR-3B return is filed.

🔹 When ITC Cannot be Claimed (Blocked Credits – Sec. 17(5))

No ITC allowed on:

-

Personal use goods/services.

-

Motor vehicles (with few exceptions).

-

Food, beverages, outdoor catering.

-

Membership of clubs, gyms, health & life insurance.

-

Works contract services (construction).

-

Goods lost, stolen, destroyed, written off.

⚠️ Example: If your company buys lunch for employees → No ITC.

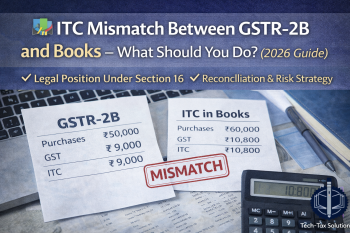

🔹 ITC Matching with GSTR-2B

-

GSTR-2B is an auto-drafted statement showing eligible ITC based on supplier filings.

-

Claim ITC only if available in 2B.

-

If invoice is missing in 2B → Follow up with supplier.

✅ Example: You purchased raw material but supplier didn’t upload invoice. You cannot claim ITC until it reflects in 2B.

🔹 Common Mistakes in ITC Claims

-

Claiming ITC on blocked credits (e.g., motor cars).

-

Claiming ITC when supplier hasn’t filed GSTR-1.

-

Booking ITC based on proforma invoice (not valid).

-

Missing reversal when goods are used for exempt supplies.

🔹 Penalties for Wrong ITC Claim

-

Interest @ 18% from date of excess claim till payment.

-

Penalty under Sec. 122 → Tax evaded or ₹10,000, whichever is higher.

-

Sec. 74A (from FY 2024-25): Unified penalty for wrong ITC, higher in fraud cases.

🔹 Best Practices for ITC Compliance

-

✅ Reconcile books with GSTR-2B monthly.

-

✅ Pay suppliers on time (within 180 days).

-

✅ Maintain proper invoices with GSTIN & HSN.

-

✅ Avoid personal/blocked expense claims.

-

✅ Conduct quarterly ITC health checks.

🔹 FAQs on ITC

Q1. Can I claim ITC on capital goods?

➡️ Yes, if used for business.

Q2. Can ITC be carried forward to next month?

➡️ Yes, unutilized ITC can be carried forward.

Q3. What if supplier files return late?

➡️ ITC will be available only when reflected in GSTR-2B.

Q4. Can I claim ITC on exports?

➡️ Yes, exports are zero-rated. ITC can be claimed/refunded.

Q5. Can ITC be claimed on expenses like office rent?

➡️ Yes, if GST invoice is in business name.

🔹 Conclusion

ITC is the backbone of GST but comes with strict rules. Claiming ITC without proper checks can lead to blocked credits, notices, and penalties. Businesses must reconcile ITC with GSTR-2B regularly and avoid blocked credits.

📌 Need expert help in ITC reconciliation or facing ITC-related GST notice?

Contact Tech-Tax Solutions – Quality, Trust & Expertise in Ghaziabad, Noida & Delhi.

%20in%20GST%20–%20Rules,%20Restrictions%20&%20Common%20Mistakes%20(2025)){kind=link}